Small Business Exits: data from November closed deals

Welcome to the November edition of Small Business Exits, the monthly publication featuring fully anonymized deal data from a selection…

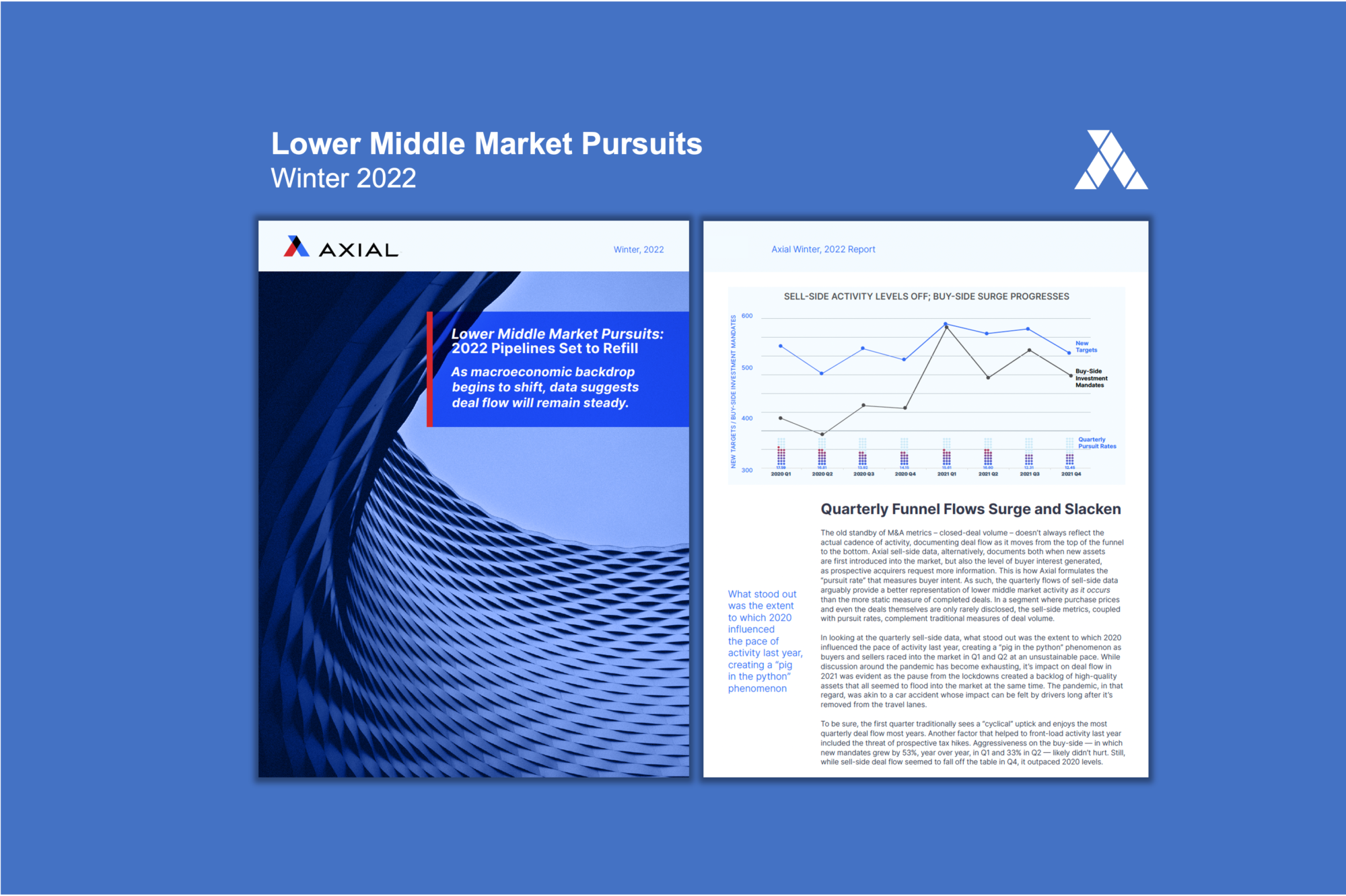

In October, we introduced a new metric – the pursuit rate – to complement existing data that buyers and sellers of lower middle market businesses traditionally rely upon, namely deal volume and EBITDA multiples. We’re not trying to re-invent the wheel. Deal totals and valuation measures, on their own, can certainly provide powerful signals depicting both the appetites of buyers and the pace of activity. In the lower middle market, however, where purchase prices and deals themselves are only very rarely disclosed, market transparency can seem fleeting.

Our latest Lower Middle Market Pursuits report, “2022 Pipelines Set to Refill,” helps to confirm our objective, which is not to replace other metrics, but rather to offer a different perspective that adds to the mosaic providing visibility into a segment that has historically been hard to read. And as our latest report shows, the lower middle market was indeed a picture of strength in 2021, even as new variables emerged.

If traditional M&A data is somewhat static (ie, closed deals aren’t reported until they actually close), Axial data, alternatively, tracks anonymized deal flow from the platform’s thousands of active members as it moves from the very top of the funnel to the bottom. And pursuit rates, which measure buyer intent, are generated as prospective acquirers request more information as deals progress further down the funnel. In addition to sell-side activity, we also track the number of new buy-side investment mandates initiated by prospective acquirers seeking very specific assets, which add further to our support pursuit rate insights.

Collectively, what this “intent” data demonstrated last year, is that both buyers and sellers are very much engaged and hungry heading into the New Year, even if appetites started to shift from the first half of last year to the second. To wit, the number of new investment targets put up for sale on the Axial platform surged by 12% in 2021, as new buy-side investment mandates ballooned by 29%, year over year.

While activity in the industrials and technology sectors fueled deal flow in the first half – and even the full year for that matter – the transportation and healthcare sectors quickly came into fashion in the second half. This was evident in both the buy- and sell-side activity. Meanwhile, the pursuit rate data suggests buyers are itching for financial services assets as well, even if the supply does not yet meet the demand.

Taken together, this activity seems to reflect awareness among buyers and sellers around both the supply chain challenges and the likelihood for interest rate increases in an inflationary environment. However, dealmaker sentiment remains as vibrant as ever.

Looking ahead, while M&A participants are certainly keeping tabs on changing macro-economic variables, anecdotally dealmakers anticipate a market environment in which deal flow continues to “normalize.” (Last year, as the report documented, saw a surge of activity in the first half that in part set an unsustainable pace but also created bandwidth challenges to complete transactions by the end of last year).

Our latest pursuits report, however, goes far deeper into these trends and others. In addition to the data, expert commentary from professionals at Auctus Capital Partners, FOCUS Investment Banking, Oberon Securities, SDR Ventures, Walnut Ridge, and Woodbridge International help provide further context. But if there is an overriding takeaway from our 2022 pursuits report, it’s that data should instill confidence in the strength and vibrancy of the lower middle market.

We hope you enjoy the report!

Click Here to Download the Winter 2022 Lower Middle Market Pursuits Report