How to Value a Heating and Air Conditioning Business + 15 Factors to Increase Value

Whether you're ready to sell your HVAC business or just assessing its worth, we break down valuation methods and key factors that can increase its value.

Consumer goods is an industry that has been through many changes in recent years. The rise of e-commerce and advancement of technology has stirred up the competition among established and growing businesses. We recently talked to three Axial members who have exposure in three sub-sectors within the consumer goods industry to hear their views on the market in 2017 and where they think the market is going in the new year.

Retail businesses have experienced a tale of two universes in 2017, said Richard Kestenbaum, a Partner at Triangle Capital.

“In one universe, there are legacy brands and retailers. They were built to do business the way that business has been done for a long time, and in a universe in which they were very successful. Now they are suffering,” said Kestenbaum. “They are suffering because business is done differently now and the values have changed”

Kestenbaum said that he has been seeing more capital raises in the middle market retail sector in 2017 because the barriers to entry have fallen and there are more opportunities for young companies seeking capital. As the old barriers to entry fallen away, there are more young companies chipping away at the large-scale established players than in the past. “As a result, the established players have lost value, and there are fewer people who are interested in acquiring them or investing in them. But there’s more interest in those younger companies with exclusive products and that have an opportunity for growth,” Kestenbaum said.

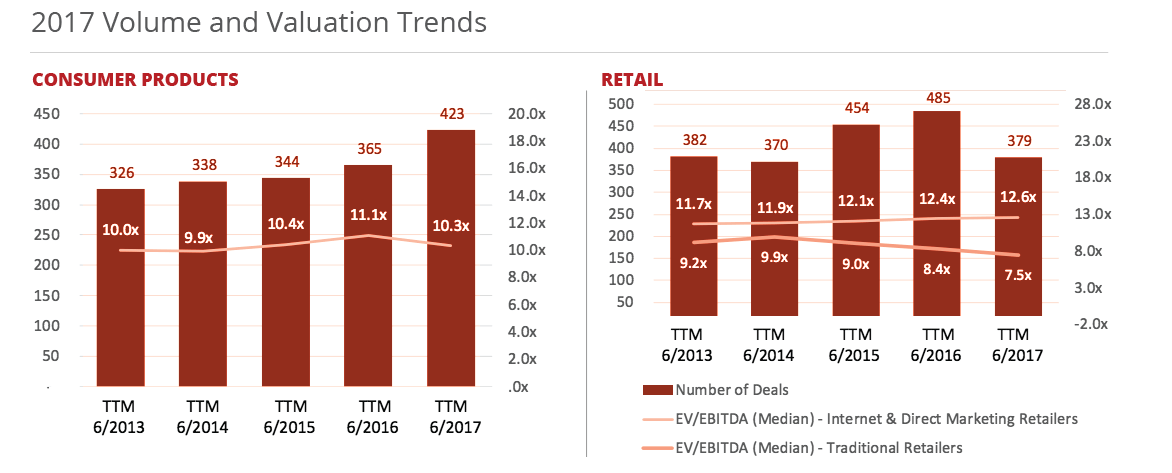

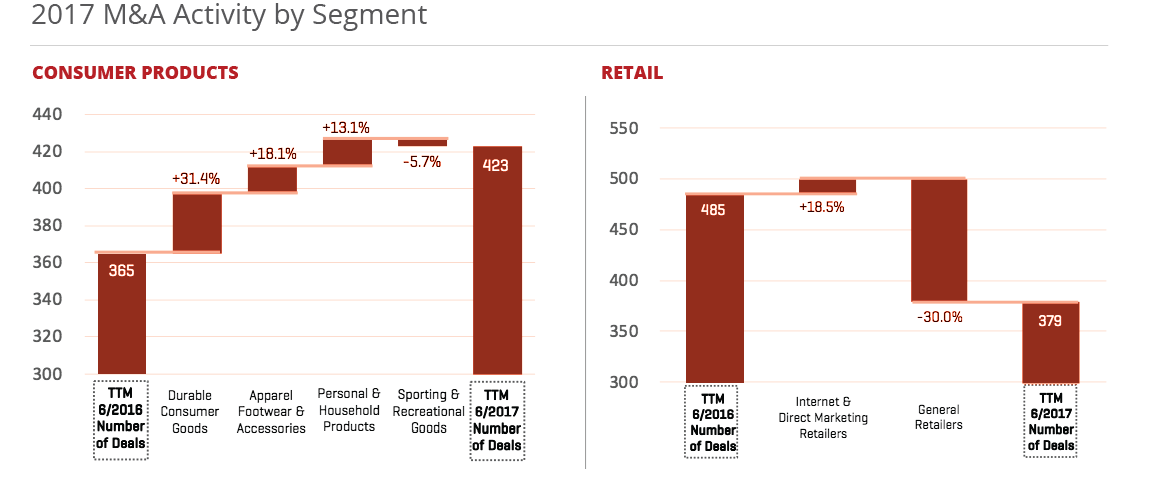

The 2017 Consumer & Retail mid-year M&A review published by Stout, an investment bank, supports Kestenbaum’s point of view. “The traditional retail side of the industry continues to struggle with increasing pressure from competitors that have more effective online shopping platforms and pricing models, agiler direct-to-consumer infrastructures, and disruptive technologies and social media outreach to capture consumers,” the report said.

The report said that traditional retail M&A activity and valuations for 2017 have declined year over year, with a shrinking number of healthy retail targets. However, demand for internet and direct marketing retailers continued to increase, with M&A activities and valuations for such companies continuing to hit all-time post-recession highs this year.

Kestenbaum said the active investors in the retail space are growth capital funds, private equity groups, and some family businesses. He said family offices are less aggressive and therefore “are not going to be the first to invest in companies that are creating changes in the industry.”

However, Anthony LeCour from Dresner Partners, a middle market investment bank, said that he expects to see more family offices investing in consumer goods in 2018, “because they have much longer hold periods, meaning they can afford to pay a higher premium, especially if they intend on using those companies as platforms to implement buy and build the strategy”. He noted that family offices might prefer companies that are considered good steady brands but not growing brands.

The DVS Group, a boutique M&A advisory firm, is currently sourcing deals in the personal care space for a family office the firm represents.

Ben Olsen, a Managing Partner at boutique M&A advisory firm The DVS Group, said his firm is speaking to a number of personal care businesses within the consumer goods industry on behalf of a family office client. Although the personal care space as a subset of consumer goods industry is a relatively new area for The DVS Group, Olsen said he has seen a healthy deal flow in the space.

The firm is actively talking to 12 business owners in the industry about a potential transaction. These owners’ businesses have EBITDA amounts ranging from below zero up to $5 million. For the smaller companies, Olsen is advising his client to offer 4x EBITDA, and for the larger businesses, he’s advising a purchase price of 4-6x EBITDA. These multiples have largely been well-received by both his client and business owners, Olsen said, but some valuation expectations are higher in cases of more established brands.

“Being small is cool right now. Small brands that have good product identity are attracting companies that are able to provide them with capital and infrastructure to get into more channels and scale,” Olsen said.

LeCour from Dresner Partners said a big trend in 2017 was that big consumer packaged goods (CPG) companies “have stepped up their efforts to invest in emerging, early-stage food and beverages companies.” Private equity firms, however, were also interested in these companies, “but since PE firms can’t extract synergies from these emerging businesses as CPGs do, they often invested more in legacy brands in order to reformulate and repackage them following a buy-and-build model.” Among corporate buyers, LeCour said that “You’ve still got low growth or no growth from all the top consumer packaged goods. So that’s Kellogg, ConAgra, Mondelez, Nestle, Unilever, and you can just go on and on. They’re still only growing 2% or even 1.5%. For that reason, big CPGs will have to purchase younger companies to foster growth.” He noted that there is around $700 to 800 billion of private equity money out there in the food and beverage sector that hasn’t been put to work.

On capital raising, LeCour said that “A lot of [the lower middle market food and beverage companies] are raising additional capital, so they’re looking to raise $20 to $40 million to really boost growth. During that process, they’ll probably end up either selling a major stake or getting sold outright, and many will choose to wait until the end 2018 when their estimated revenues will warrant a higher valuation.”

He also added that a lot of the established lower middle market food and beverages companies will trade at about 8 to 10 times EBITDA, which are lower multiples than high growth, emerging brands.