The Middle Market Review Insights on the Middle Market.

Thanks for subscribing!

Size Matters: 4 Middle Market M&A Trends

Our friends at GF Data Resources (GFDR) recently released their 2Q 2011 Middle Market Report. GFDR provides data on middle market and lower middle market private equity sponsored M&A transactions with enterprise values of $10 to 250 million. The report indicates that the “size premium” – the premium investors are willing to pay for the inherent safety of a larger business – is an increasingly important driver of middle market M&A valuations. Activity on the Axial network provides additional evidence to support this trend. The prevalence of an increasing size premium could have several implications for the private middle market M&A environment.

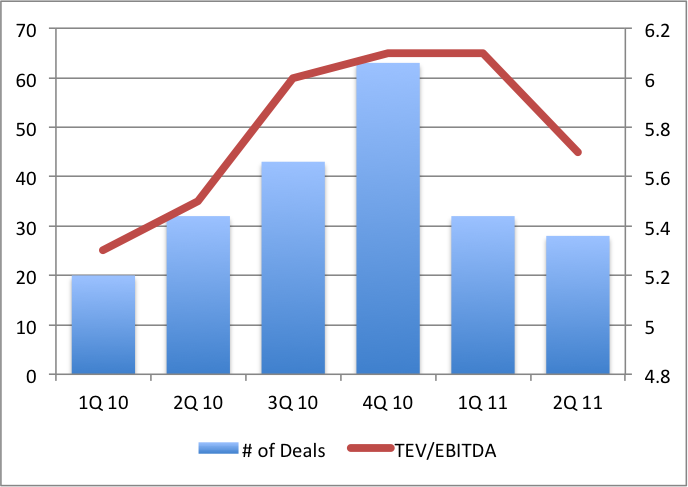

GFDR noted that, based on 60 completed transactions in the first half of 2011, while overall valuations were relatively stable at 5.8x trailing twelve months (TTM) EBITDA, there was a growing disparity in the multiples paid for businesses of different scale. Companies with total enterprise values (TEV) of $100-$250 million fetched an average 7.5x TTM EBITDA, while those with TEV of $10-$25 averaged 5.2x. Furthermore, the average valuation of 7.5x for larger middle market deals reflected more than a full turn increase when compared to the prior year’s 6.2x. GF Data’s founder and CEO, Andrew T. Greenberg, commented that, “[GF Data] began this year by predicting that the story of middle market deal activity in 2011 would be a resurgent premium for greater deal size joining the premium for better deal quality as a driver of value. As predicted, size premium is now driving the market.”

Axial has observed similar M&A trends in the appetite for larger deals. In the first seven months of 2011, acquisition opportunities for businesses with more than $5 million of EBITDA have generated more than 3x the interest of those with less than $5 million. Over the same period, companies with more than $10 million of EBITDA generated more than 2x the interest of those with less than $10 million. Given the data supporting these trends, it is a good time to consider the potential implications of this shift in demand for privately held, middle market companies. A premium on size likely reflects a premium on safety and increasing caution towards the macro-economy. If this is the case, we highlight a number of possible trends to watch for going forward:

- This trend could lure more strategics into the market as they benefit from the buffer of their base business and the potential to realize synergies post-acquisition. By combining acquired assets with their existing businesses, strategic acquirers are able to accept more near-term uncertainty in the operating environment. Furthermore, strategic buyers are better positioned to reduce this uncertainty given their operating expertise and ability to eliminate certain redundant overhead costs.

- For the same reasons that would attract strategic acquirers, financial buyers might be inclined to make acquisitions through their portfolio companies and engage in “add-on” or “roll-up” strategies. The combination of smaller assets makes them safer, and these sponsors will be further along the ‘learning curve’ in their respective industries.

- Similarly, private equity sponsors with significant experience or expertise in a specific industry might be favored, as sellers and their advisors seek investors that have a differentiated perspective and/or can add the most value…and are willing to reflect that in their terms. Even if a financial buyer lacks a strategic ‘platform’ from which to make an acquisition, a successful track record with similar transactions is likely to be a differentiating factor in competitive processes.

- Transaction terms might also adapt to bridge the valuation and financing gaps at the lower end of the middle market. An increase in earnouts and seller financing are the most likely levers to be pulled. In a June 23 post, GFDR’s Greenberg pointed out that, “Seller financing or earnouts (let’s call them SFEs) were reported in 70% of deals completed in Q1 [2011] in the $10-25 million value range, compared to 27% in the balance of the sample,” and that, “Since 2006, SFEs figured in 45% of deals completed in the $10-25 million TEV tier, compared to 35% of deals in the balance of the TEV range [GF Data] cover[‘s] (that is, $25 to 250 million).”

As the macro-economic climate remains uncertain at best, we would expect the private middle market M&A environment to be increasingly dynamic. The evidence for an increasing size premium is compelling, and its incidence has material implications for all middle market participants.

Deal Sourcing Takeaway for Bankers and Business Owners: make sure you and your clients understand these trends in the context of valuation expectations and that you approach the right buyers given the size of the business being sold.

Deal Sourcing Takeaway for Buyers: if you’re focused on acquiring businesses with greater than $5M of EBITDA, the data suggests that competition is intensifying; more nimble buyers may seek sub-$5M EBITDA opportunities to improve their chances of obtaining proprietary deal flow or gaining an edge over other less flexible buyers.

Learn More About Joining Axial

Subscribe to Middle Market Review