Advisor Industry Awards: The Top 12 Deals of 2024

Axial first introduced quarterly League Tables in 2019 to recognize the top Investment Banks and M&A Advisory Firms on Axial…

Technology remains a steady presence in the lower middle market, representing ~13% of deals brought to market via Axial over the past year. The technology vertical has consistently ranked in the top three for pursuit rate—claiming the number one spot for half of 2024, as highlighted in our quarterly series, The SMB M&A Pipeline. This steady momentum underscores the sector’s resilience and strong investor and advisor interest.

For a glimpse into how technology deals are getting structured in the lower middle market, this below snapshot from Axial’s Winning LOI Hub features a selection of executed LOIs from technology deals, offering a look at key deal terms in the sector.

| Deal Headline | Revenue | EBITDA | Multiple* | Cash | Earnout | Rollover Equity | Seller Note |

|---|---|---|---|---|---|---|---|

| Food & Bev. eCommerce | $12,700,000 | $2,310,000 | 8.40x | 58.76% | 15.46% | 25.77% | -- |

| IT Software Services | $4,600,000 | $1,700,000 | 7.36x | 46.20% | 8.50% | 37.80% | 7.50% |

| IT Infrastructure Software | $7,230,000 | $1,800,000 | 5.23x | 70.00% | -- | -- | 30.00% |

| Healthcare Software | $3,600,000 | $2,500,000 | 4.00x | 75.00% | -- | -- | 25.00% |

| IT Hosting Services | $6,720,000 | $1,425,000 | 5.11x | 84.78% | 15.22% | -- | -- |

Today, Axial is excited to release its 2025 publication of the Top 50 Lower Middle Market Technology Investors and M&A Advisors: a list that features Axial’s 50 most active and sought-after members who specialized in transactions across various tech sectors over the past 12 months (methodology below). In addition to celebrating these Top 50 members, this feature includes reflections and insight from our recent Top 50 Technology M&A Outlook survey.

Our Top 50 technology list was generated based on a weighted formula leveraging four key metrics:

Congratulations to these members for their achievements!

We asked deal professionals whose firms are featured on this list to share insights on the general industry landscape, business owner mentality, and key sub-sectors, including:

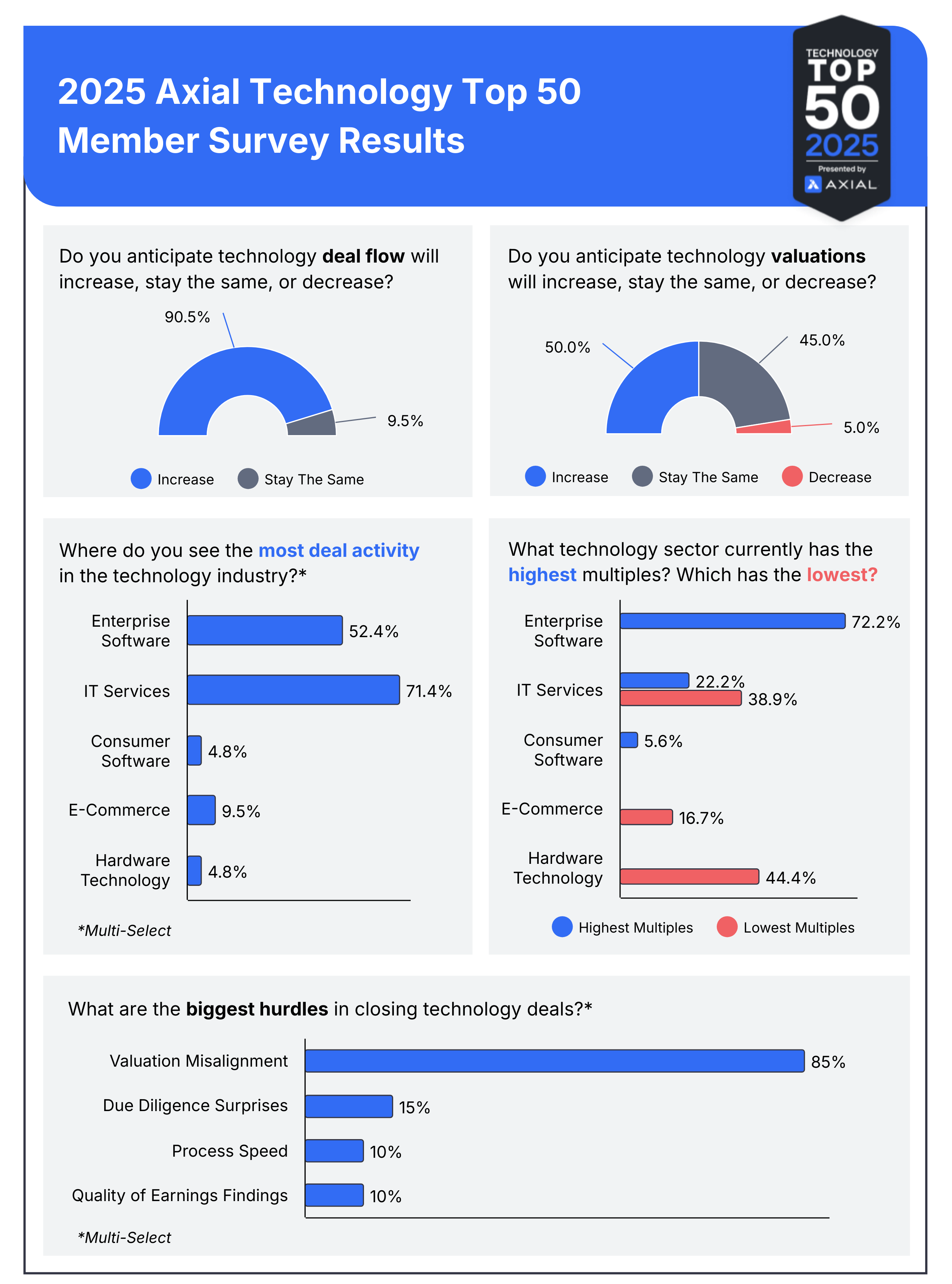

Of the survey respondents — a combination of both the buy- and sell-side — 68% of them closed three or more deals in the technology space in the past 12 months.

As can be seen in the chart, deal professionals are most bullish on enterprise software and IT services. Outside of those two standout spaces, eCommerce, consumer software, and hardware technology all received honorable mentions.

Drilling down a bit deeper, managed service providers and cybersecurity were the most frequently mentioned verticals when respondents were asked about the sub-sectors with the highest amount of deal activity. Runners-up included channel partners, software development tools, and artificial intelligence.

Highest Multiples

Enterprise software led all sectors in terms of valuation confidence, with respondents estimating that these businesses consistently bring EBITDA multiples of 10-14x in today’s market. According to Stan Gowisnock, Chief Strategic Advisor and Technology Services Team Leader at FOCUS Investment Banking, “Enterprise software continues to receive attractive valuations because of the ability to scale quickly and drive profitability within a short amount of time.”

Mid-Range Multiples

IT Services fell into the “highest multiple” category for some respondents, while a number of others dropped this sector into the “lowest multiple” category. As Dylan Tober of ITExchangeNet remarked, “[The multiple] is completely dependent on recurring revenue, margins, and customer retention.”

Because of the wide range of service offerings associated with IT Services businesses, the average EBITDA multiple range was a bit wider in this sector, spanning 4-10x.

Lowest Multiples

Hardware technology was most often referenced in the “lowest multiple” category; almost half of respondents said that they would expect a 2-6x EBITDA multiple in this sector, depending on the business.

FOCUS’ Gowisnock commented: “We continue to see downward pressure on hardware tech multiples due to the inherent cost built into hardware businesses and the levers owners have to pull to optimize efficiency and profitability. With that said, buyers in this space are still active, and sellers in this space can expect active processes with a number of different buyers.”

While the biggest hurdle in actually closing technology transactions is relatively straightforward, the list of broader challenges across the industry is a bit more nuanced.

Artificial intelligence, cybersecurity, and talent are three things that came up time and time again in our member insights. And one thread that was consistently referenced in connection to all three of those things? Government regulation and uncertainty.

Artificial Intelligence

While many are excited about the opportunities within the reach of AI, plenty of unknowns still provide pause, especially in the M&A space.

How do you underwrite it? How deeply will it disrupt incumbent software businesses? Who is adopting it… and how? Which companies will be displaced? How will it be regulated? And how will those regulations affect businesses becoming more reliant on it?

There are a myriad of questions that buyers are asking right now, and the market doesn’t yet have the answers. So, while AI is one of the most commonly referenced opportunities in the industry, it’s just as commonly referenced as a major challenge for buyers and sellers alike.

Cybersecurity

There are countless cybersecurity concerns for businesses in our technology-driven world, from compliance issues and overburdened teams to data privacy, threats and breaches.

And when it comes to M&A – more specifically, add-on acquisitions – buyers need to be cognizant of changing (or merging) IT systems. Different systems with varying security standards or protocols can create vulnerabilities and gaps in protection.

Talent

Finding and retaining talent – especially the right talent – is not an easy feat right now. Uncertainty around immigration and H1B Visas further adds to this concern.

However, there may be a silver lining; while there are plenty of reasons why owners and operators may be concerned about staffing, the high number of government layoffs may actually provide an influx of highly skilled technology talent, so stay tuned.

| Current M&A Technology Opportunities |

|---|

| Where others are not looking! Away from anything AI, away from data. These areas are indeed exciting but very expensive and likely overpriced if we revisit deal terms in 2025 2026, and 2027. Similar to 2022, pricing for deals looked very expensive in hindsight upon revisiting in 2024. David Eshaghian, Panther Equity |

| AI represents a huge opportunity. The ability to do the work of several people with a handful of AI tools represents an enormous accelerant. Those who are able to properly leverage it to drive results efficiently are going to reap huge rewards. Dennis Huang, Polychrome |

| Cloud, cyber, and of course, AI. Nearshore and offshore are growing in importance in the infrastructure/MSP space. And consolidation in the MSP space. Cristian Anastasiu, Excendio Advisors |

| Innovation and healthcare data. Neil Johnson, Lawrence, Evans & Co. |

| Gen AI replacing many routine tasks, jobs, and programming. Pundi Narasimham, STS Worldwide |

| Cybersecurity services and AI... once users embrace and learn how to leverage operational efficiencies. Tim Mueller, IT ExchangeNet |

| Autonomous enterprise IT development. Reginald McGaugh, Cornhusker Capital |

| Mass layoffs in government will create a lot of tech talent looking for jobs and creating new businesses. Peter Formanek, Young America Capital |

| AI and overseas talent. Charles Scripps, Blacklake Capital |

| Consolidation within fragmented markets, using AI tools to build services firms, and using the sales, rev ops, and marketing tools emerging before our eyes. Ryan Barnett, Revenue Rocket Consulting Group |

![]()

Our Top 50 technology list was generated based on a weighted formula leveraging four key metrics:

The number of technology deals brought to market via Axial (sell-side)

The level of interest those deals generated from Axial’s buyside member base

The number of specific technology-focused investment mandates created in the platform (buyside)

The number of technology deals that progressed through the deal funnel achieving a signed NDA, shared CIM, received IOI, received LOI, executed LOI, or successfully consummated transaction (buyside & sell-side).