The Winning M&A Advisor [Vol. 1, Issue 5]

Welcome to the latest issue of The Winning M&A Advisor, the Axial publication that anonymously unpacks data, fees, and terms…

Tags

Bain’s annual in-depth recap of the year in M&A is now out. Because Bain is decidedly “up-market” from the lower middle market M&A and private equity universe, many of Bain’s clients are the ultimate acquirers of businesses that are developed, grown and professionalized by lower middle market business owners and their private equity partners.

Knowing how this up-market set of acquirers make dealmaking and strategic M&A decisions is a helpful input to your exit strategy.

If you own one or more lower middle market businesses with a potential to generate $10M of EBITDA or more in the coming three years, this piece is especially for you.

Herewith, three takeaways from the report.

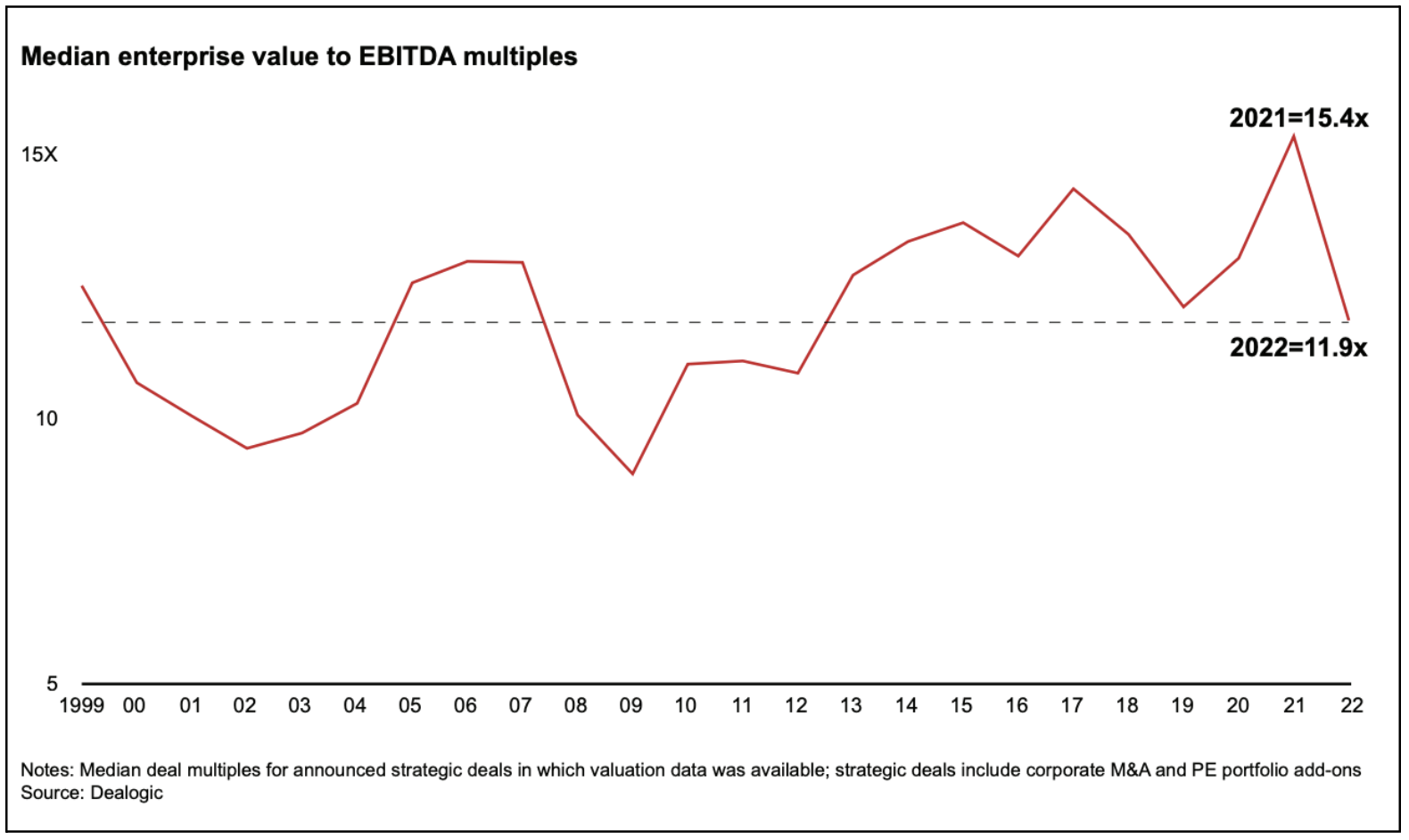

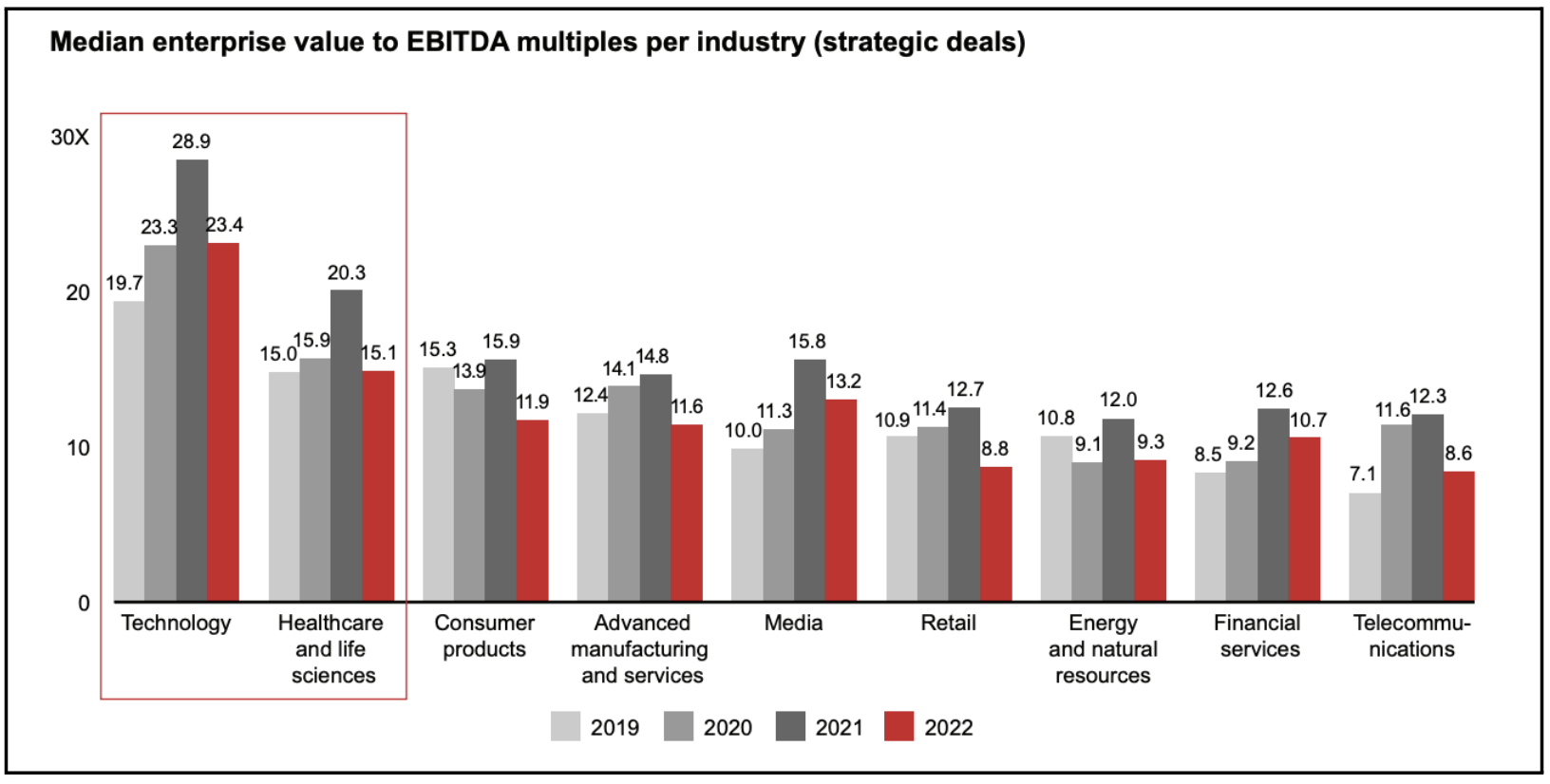

It took only one page for the writers to deliver the punchline: valuations are down big. On average, they’re down 22% for 2022’s strategic (only PE add-ons and corporate acquirers) M&A deals. It’s certainly possible that “non-strategic” M&A had an even more precipitous fall than that given all the headwinds that emerged.

Unlike in other M&A markets where multiple contraction was concentrated in a few sectors, multiple contraction in the 2022 M&A market was universally distributed.

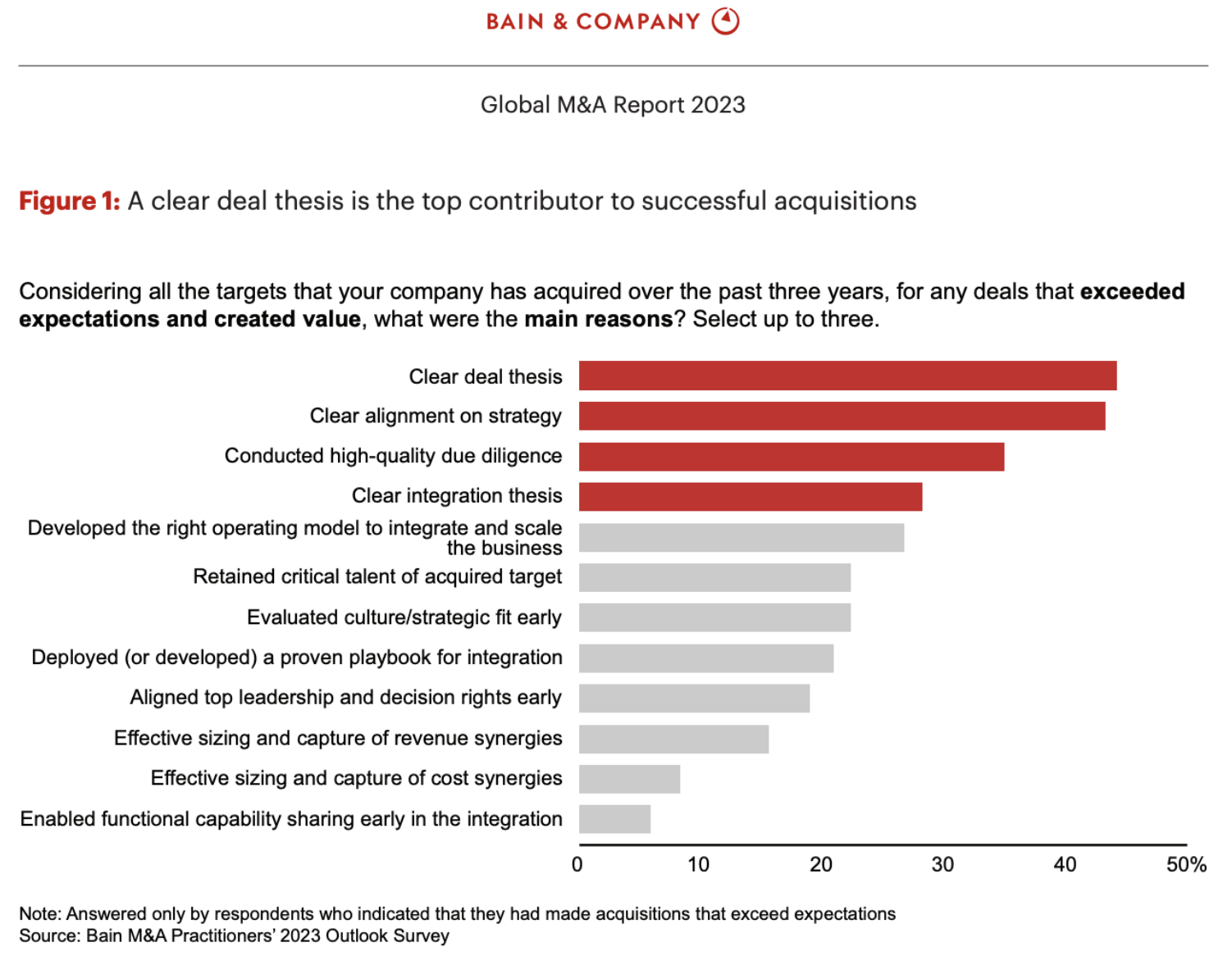

“Having a clear deal thesis” going into an acquisition was the top driver of M&A outperformance according to respondents to Bain’s survey. As such, business owners exploring an exit for their lower middle market business should be keenly evaluating acquirers based on the acquirer’s ability to articulate their “WHY”. If you aren’t hearing compelling reasons and perspectives, they’re likely not the ideal buyer. The best way to get good at assessing the “WHY” of various acquirers is unsurprisingly by meeting with many of them.

Take a look at the chart below that Bain supplies. Top reasons for a great deal start with a great “WHY” but also critically require good alignment, a good diligence process, and a clear plan for what will be done post-transaction. You should push for satisfactory answers on all of these items.

Culture is often incorrectly viewed as an ephemeral and elusive intangible aspect of an organization. This mischaracterization often lowers the expectations sellers and acquirers place upon themselves to perform for high quality cultural due diligence in this area. Avoid this mistake.

The Bain report does a nice job making more concrete how both sellers and buyers can perform cultural due diligence on the other. They mention three areas:

As the owner of the business, consider your organization’s purpose and values, and think through examples of how those values have been used to make decisions and guide the company. Perhaps they’ve guided how you’ve thought about offshoring, layoffs, compensation, benefits, workmanship, customer orientation.

Going through a similar exercise in which you examine how you presently make decisions will also be helpful. Is it top down, bottoms-up, a mix? Is there a methodology that is adhered to? Having a clear understanding of how your organization currently makes decisions helps you as you ask the same question of different acquirers. And be prepared to hear a range of both acceptable or unacceptable answers on this question.

The Bain M&A report is a helpful annual survey of how the larger-cap M&A players think and do business. Business owners may think it’s a report that’s only interesting for EBITDA-obsessed dealmakers. That would be wrong. If you’re exploring an exit in the coming years, the report is a credible way to get to know more about your dance partners in advance of the real dance.